It was a bullish week for US equity indexes, with net weekly gains ranging from +7.5% (Nasdaq comp'), +6.4% (SPX), +6.0% (R2K), +5.4% (Dow), +5.3% (Trans), to +5.1% (NYSE comp')

Lets take our regular look at six of the main US indexes

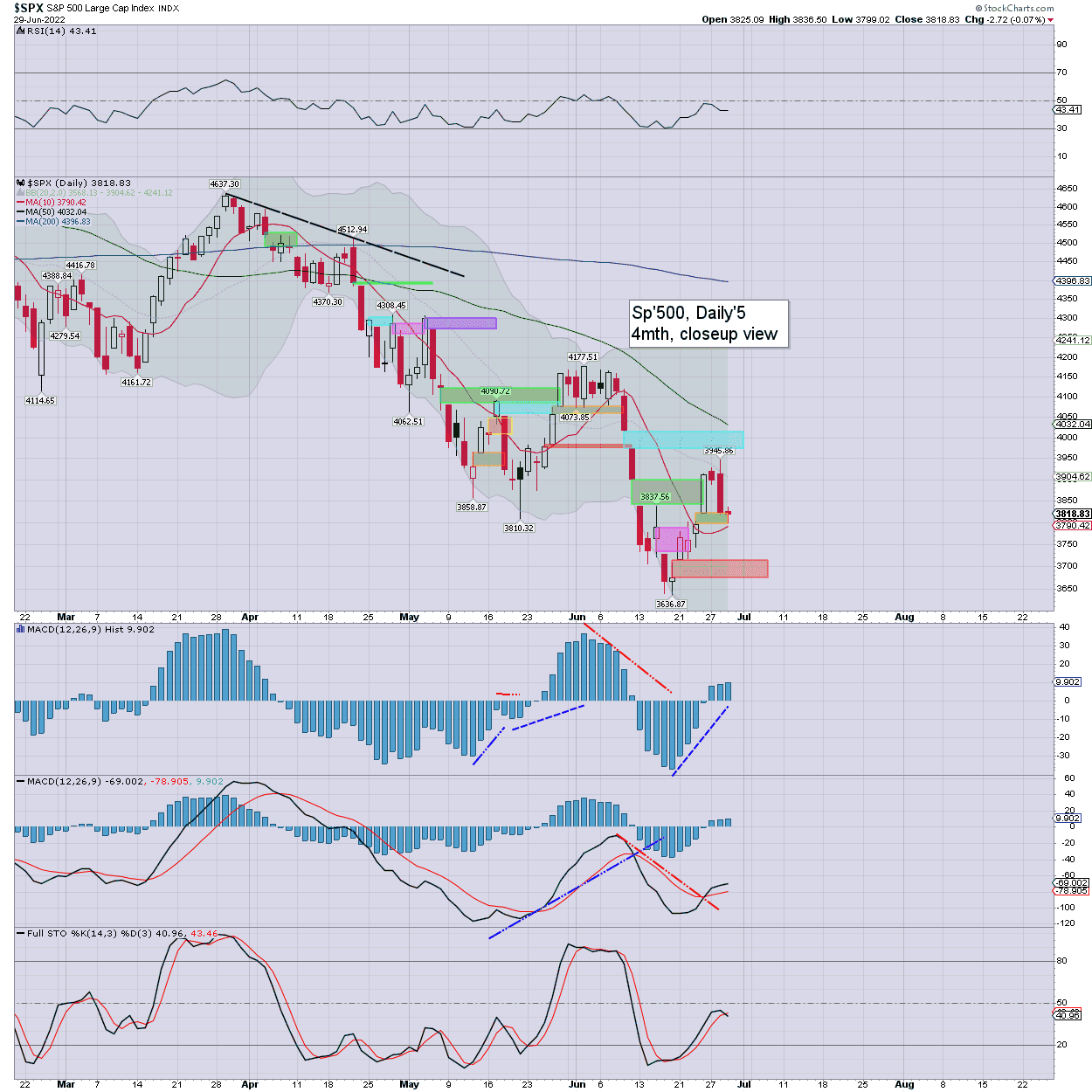

sp'500

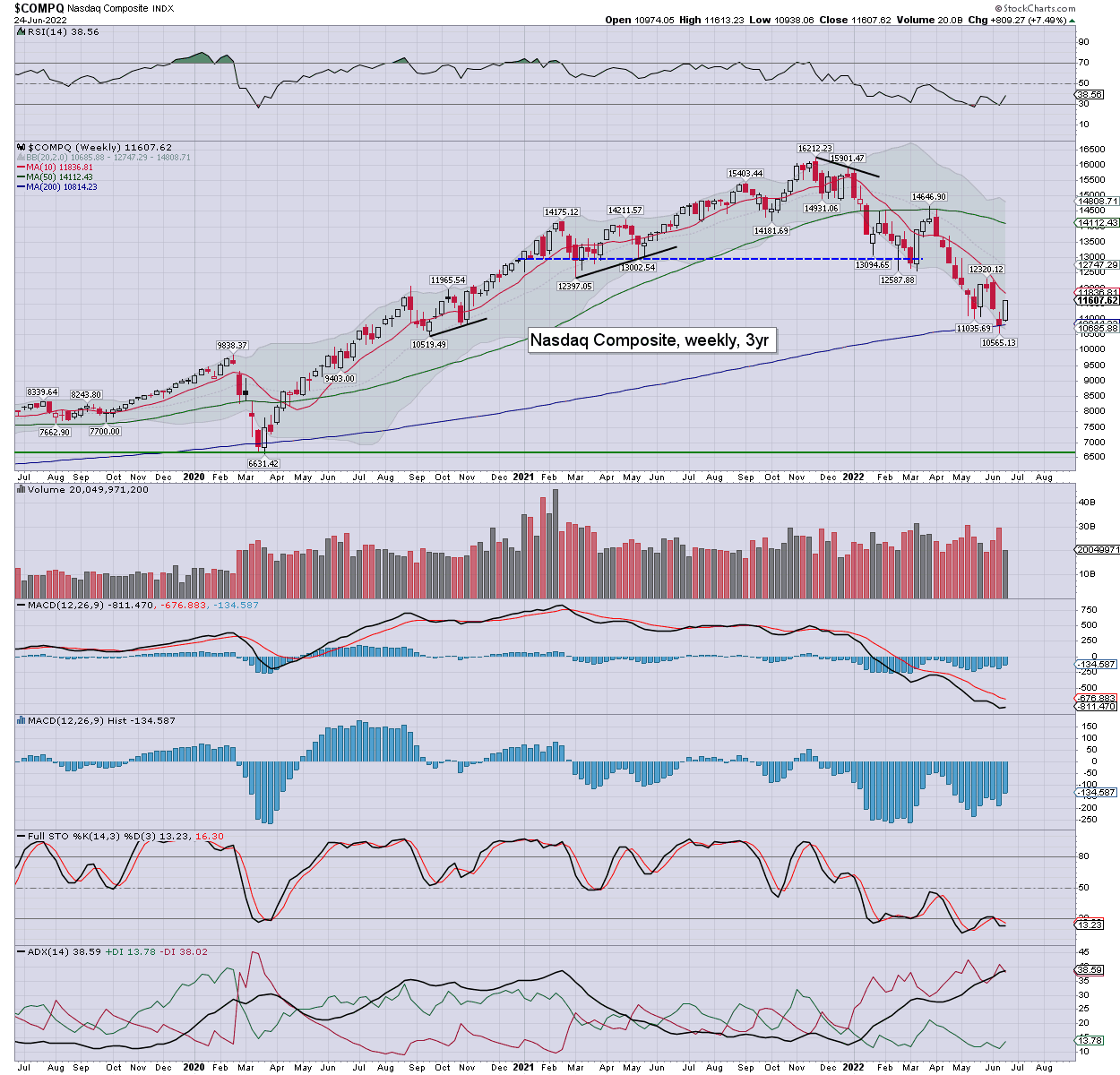

Nasdaq comp'

Dow

R2K

NYSE comp'

Trans

–

Summary

All six US equity indexes settled net higher for the week.

The Nasdaq comp' lead the way higher, whilst the NYSE comp' was the laggard.

More broadly, all six US equity indexes are trading under their respective monthly

10MA, and have increasingly negative momentum. By definition, all six

indexes are m/t bearish.

–

Looking ahead

Earnings:

M - NKE

T -

W - BBBY, GIS, PAYX, NG

T - WBA, STZ, AYI, MU

F -

-

Econ-data/events

M - Durable goods orders, pending home sales

T - Intl' trade, Case-Shiller HPI, consumer conf'

W - Q1 GDP (print'3), EIA Pet'

T - Weekly jobs, pers' income/spending, Chicago PMI

F - ISM/PMI manu', construction

*As Thursday is end month, Q2, and the first half, I'd expect more dynamic price action on very high volume.

**With Monday July 4th CLOSED for Independence Day, the preceding Friday will be inclined for subdued trading on very light volume.

-

Final note

A bullish week, but do you believe sp'3636 is a key mid term floor? Have you seen capitulation yet? Sure... you could argue some of the ex-hysteria stocks - such as RBLX, have floored, but the main market doesn't look like it has.

The equity bulls have two monstrously problematic data points ahead in July. The first is the next CPI (due July 13th), and that should remain hot. The second is Q2 GDP (due July 28th), which should confirm the US economy has been in recession since January.

Its extremely difficult to see the market not breaking new cycle lows in July, with both of those econ-data points set to remind the mainstream cheerleaders and 'smart guy' analysts that things are increasingly difficult.

There are just so many other problems out there, not least fertiliser and crop yields, which appear set to decline for some years. Ohh, and what about the Diesel and DEF issue? I'd hope most of you are aware of the latter.

Regardless of how June settles, July/Q3/H2, should see further market drama, but hey... who doesn't love some drama?

For more of the same... well, you know where to find me.

For details and the latest

offers, see: https://www.tradingsunset.com

Have

a good weekend

--

*the next post on this page will likely appear 5pm EST on Monday.