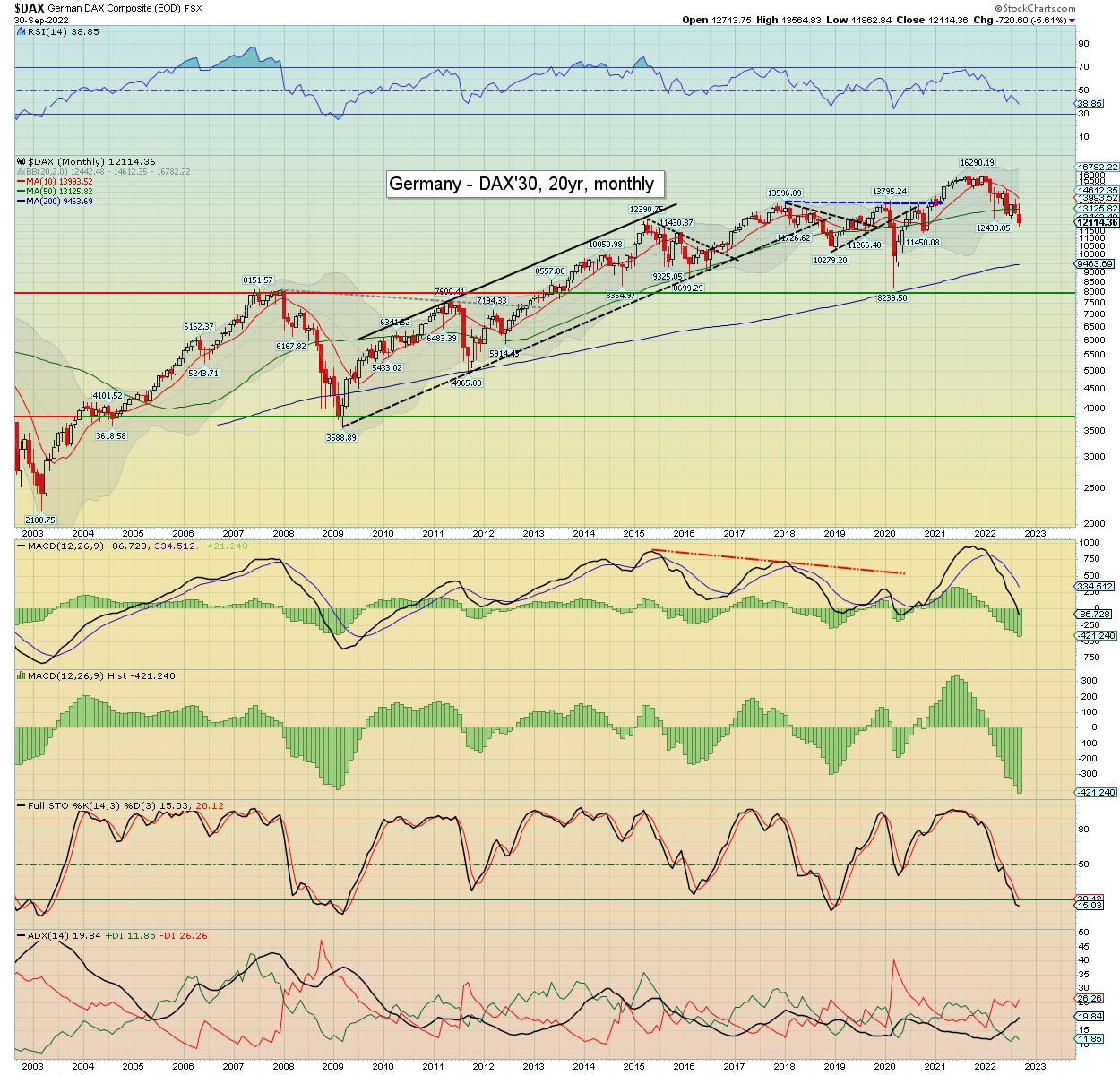

It was a bearish month for most world equity markets, with net monthly changes ranging from -16.1% (Russia), -13.7% (Hong Kong), -8.8% (USA), -7.8% (Australia), -7.7% (Japan), -5.6% (Germany), -5.5% (China), 5.1% (South Africa), -3.5% (India), to +0.5% (Brazil).

Lets take our regular look at ten of the world equity markets.

USA - Dow

Germany – DAX

Japan – Nikkei

Brazil – Bovespa

Russia - RTSI

India – SENSEX

China – Shanghai comp'

South Africa – Dow

Hong Kong – Hang Seng

Australia – AORD

–

Summary

Nine world equity markets were net lower for September, with one net higher.

Russia and Hong Kong lead the way down, whilst Brazil managed a moderate gain.

Eight world equity markets settled under their respective monthly 10MA, the two exceptions being Brazil and India.

All ten world equity markets have negative monthly price momentum, as the collective of world equity markets are in a bear market.

-

Looking ahead

Earnings:

M -

T - AYI, NG

W -

T - STZ, MKC, CAG, ANGO, LEVI, ACCD

F - TLRY

-

Econ-data:

M - PMI/ISM manu', construction, vehicle sales

T - JOLTS, factory orders

W - ADP jobs, Intl' trade, pending home sales, PMI/ISM serv', EIA Pet', OPEC+ meeting

T - Weekly jobs

F - Monthly jobs, wholesale invent', consumer credit

--

Final note

The system is breaking apart. This past week saw the BoE spool up the printers to buy bonds, effectively bailing out the UK pension industry. Its a typical can kicking measure, and will do nothing to solve the underlying problems.

The UK sheep are increasingly stressed, as power prices are adjusting (as of Oct'1st). Many will manage... some won't. Then there are the higher mortgage repayments. Again, many will manage... some won't. It doesn't take more than a small percentage of defaults to collapse a ponzi-based financial system.

I'd understand that most of you don't care about the UK, but its reflective of mainland Europe, and to some extent, the USA. Never mind the issue that a spiraling Pound (and Euro) will pressure the dollar upward, and we know what that does to most asset classes, right?

It should be clear, we're just in the early phase. We've not even seen the leading edge of consumer debt defaults yet. How long until that occurs? A few months, six, a year?

The window has closed

Across the summer I've noted the 'window of opportunity' to prepare for the winter of 2022/23. That window has now closed. Either you're ready... or you're not.

October, and the bulk of Q4 should be 'scary wild' in the US and broader global capital markets. If you're interested in non-sugar coated chatter, then you know where to find me.

Have a good weekend

--

*the next post on this page will likely appear 5pm EST on Monday.