It was a bullish month for most world equity markets, with net monthly changes ranging from +3.7% (Russia), +3.6% (India), +2.9% (Japan, South Africa), +2.5% (USA, Brazil), +1.9% (Germany), +1.7% (Australia), +1.5% (China), to -2.5% (Hong Kong).

Lets take our regular look at ten of the world equity markets.

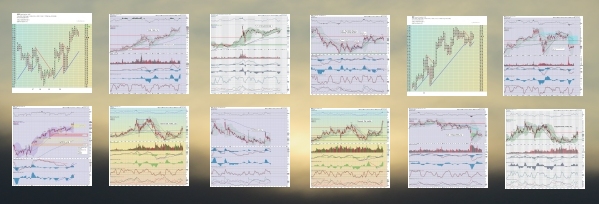

USA - Dow

Germany – DAX

Japan – Nikkei

Brazil – Bovespa

Russia - RTSI

India – SENSEX

China – Shanghai comp'

South Africa – Dow

Hong Kong – Hang Seng

Australia – AORD

–

Summary

Nine world markets settled net higher for April.

Russia was the strongest market, whilst Hong Kong was the weakest.

Eight world markets are trading above their respective monthly 10MA, the two exceptions being Brazil and Russia.

Germany, China, South Africa, and Hong Kong, have net positive monthly momentum.

Germany, India, South Africa, and Australia aren't far from breaking new historic highs.

-

Looking ahead

Another very busy week is ahead, with a truck load of earnings, an FOMC, and a fair amount of econ-data.

Earnings:

M - SOFI, NCLH, ON, MGM, RIG, FANG, CAR, NXPI, CF, CHGG

T - PFE, UBER, BP, MAR, MPC, STNG, LNG, CEIX, AMD, F, ET, SBUX, MTCH, CZR

W - CVS, YUM, GOLD, PSX, GNRC, EL, WWE, SPWR, QCOM, ALB, SEDG, MELI, FSLY, MRO, ETSY

T - MRNA, BUD, RCL, PTON, DDOG, COP, SHEL, APA, AAPL, SHOP, SQ, COIN, DKNG, LYFT, FTNT, CVNA, BKNG

F - AMC, WBD, FUBO, EOG, CI, ENB, INSW, GSAT

-

Econ-data:

M - PMI/ISM manu', construction

T - JOLTS, factory orders

W - ADP jobs, PMI/ISM serv', EIA Pet' report

*FOMC announcement 2pm, with a press conf' at 2.30pm. Rate hike ten of 25bps to 5.00-5.25% can be expected.

T - Weekly jobs, Productivity, Intl' trade

F - Monthly jobs, consumer credit (3pm)

--

If you value my work, subscribe to my intraday service.

For

details, and the latest offers: https://www.tradingsunset.com

Have a good weekend

--

*the next post on this page will likely appear 5pm EST on Monday.